Understanding Your Car Insurance Policy: A US Guide

Decoding Car Insurance Basics Understanding Coverage Types

Okay, let's dive into the wild world of car insurance! It can seem like a confusing maze of terms and conditions, but don't worry, we'll break it down. First things first, you need to know the different types of coverage you can get. Think of it like choosing different superpowers for your car – each one protects you in a specific situation.

Liability Coverage: This is the most basic type and usually required by law. It covers the damages you cause to someone else if you're at fault in an accident. So, if you rear-end someone, your liability coverage pays for their car repairs and medical bills. There are two parts to liability: Bodily Injury Liability (BI) and Property Damage Liability (PD). BI covers injuries to others, and PD covers damage to their property (like their car or fence).

Collision Coverage: This covers damage to your car if you hit another vehicle or object, regardless of who's at fault. So, if you accidentally back into a pole, collision coverage will help pay for the repairs. It’s often subject to a deductible, meaning you pay a certain amount out of pocket before the insurance kicks in.

Comprehensive Coverage: Think of this as protection against everything *other* than collisions. It covers things like theft, vandalism, fire, hail, floods, and even hitting a deer. Basically, if something happens to your car that isn't a crash with another vehicle, comprehensive coverage likely has you covered. Like collision, it often has a deductible.

Uninsured/Underinsured Motorist Coverage: This is super important! It protects you if you're hit by someone who doesn't have insurance or doesn't have enough insurance to cover your damages. It can cover your medical bills, lost wages, and even pain and suffering.

Personal Injury Protection (PIP): This coverage, available in some states, covers your medical expenses and lost wages, regardless of who's at fault in an accident. It can also cover your passengers.

Navigating Car Insurance Quotes Finding the Best Rates

Alright, now that you know the different types of coverage, let's talk about getting quotes. The price of car insurance can vary *wildly* depending on several factors. It's like trying to predict the weather – there are so many variables!

Factors Affecting Your Premium: Your age, driving record (tickets and accidents), the type of car you drive, your location, and even your credit score can all impact your premium. Younger drivers and those with a history of accidents will generally pay more. Living in a densely populated area with high crime rates can also increase your rates.

Shopping Around: The best way to find the best rates is to shop around and get quotes from multiple insurance companies. Don't just stick with the first quote you get! Websites like Compare.com, The Zebra, and Insurify can help you compare quotes from different insurers.

Bundling Policies: Many insurance companies offer discounts if you bundle your car insurance with other policies, like homeowners or renters insurance. This can save you a significant amount of money.

Raising Your Deductible: Increasing your deductible (the amount you pay out of pocket before insurance kicks in) can lower your premium. However, make sure you can afford to pay the higher deductible if you need to file a claim.

Discounts: Ask about potential discounts! Many insurers offer discounts for things like being a safe driver, having anti-theft devices in your car, being a student, or being a member of certain organizations.

Understanding Policy Language Deciphering the Fine Print

Okay, this is where things can get a little tricky. Car insurance policies are filled with legal jargon, but it's important to understand what you're signing up for. Don't be afraid to ask questions if you don't understand something!

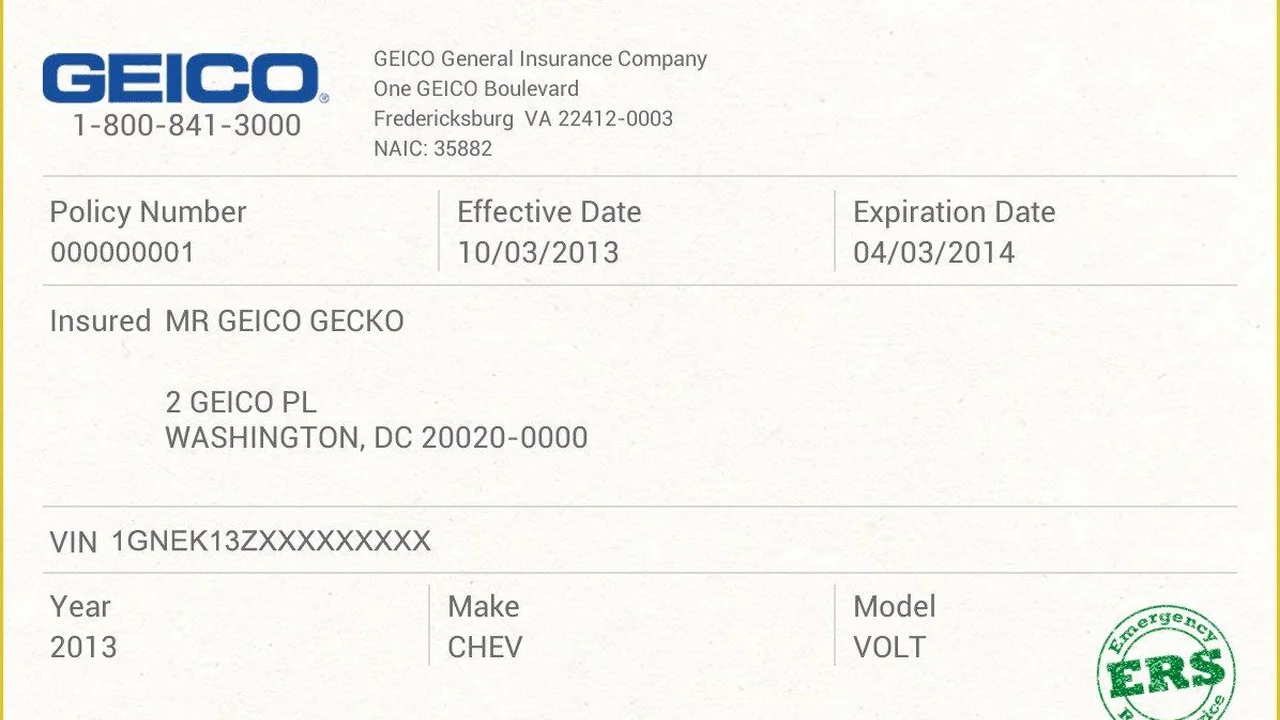

Policy Declarations Page: This page summarizes your coverage and lists your policy limits, deductibles, and other important information. It's basically the cheat sheet for your policy.

Definitions: Pay attention to the definitions section. It defines key terms used throughout the policy. For example, it will define what "bodily injury" and "property damage" mean.

Exclusions: This section lists the things that your policy *doesn't* cover. For example, most policies exclude coverage for intentional acts, like intentionally damaging someone else's car.

Conditions: This section outlines your responsibilities as a policyholder. For example, it will explain how to file a claim and what information you need to provide.

Limits of Liability: This is the maximum amount your insurance company will pay for a covered claim. Make sure you have enough coverage to protect yourself from potential lawsuits.

Filing a Car Insurance Claim A Step by Step Guide

So, you've been in an accident. Now what? Filing a car insurance claim can seem daunting, but here's a step-by-step guide to help you through the process:

1. Report the Accident: Immediately report the accident to your insurance company. Provide them with as much information as possible, including the date, time, and location of the accident, as well as the names and contact information of the other driver and any witnesses.

2. Document the Damage: Take photos or videos of the damage to all vehicles involved. Also, take photos of the accident scene, including any skid marks, debris, or traffic signals.

3. Exchange Information: Exchange insurance information with the other driver, including their name, address, phone number, insurance company, and policy number.

4. File a Police Report: If there are injuries or significant damage, file a police report. This will help document the accident and provide valuable information for your insurance claim.

5. Cooperate with the Insurance Company: Cooperate with your insurance company's investigation. They may ask you to provide additional information, such as medical records or repair estimates.

6. Get an Estimate: Get an estimate from a reputable auto repair shop. Your insurance company may have a preferred repair shop, but you have the right to choose your own.

7. Review the Settlement Offer: Once the insurance company has completed its investigation, it will make a settlement offer. Review the offer carefully and make sure it covers all of your damages. If you're not satisfied with the offer, you can negotiate with the insurance company.

Car Insurance Products Recommendations and Comparisons

Let's talk about some specific car insurance products and how they stack up. Keep in mind that the best product for you will depend on your individual needs and circumstances.

Product Recommendation 1: Progressive Snapshot Safe Driving Program

Description: Progressive Snapshot is a usage-based insurance program. You plug a small device into your car, and it tracks your driving habits, such as speeding, hard braking, and nighttime driving. If you're a safe driver, you can earn significant discounts on your premium.

Use Case: Ideal for drivers who are confident in their safe driving habits and want to potentially save money on their insurance.

Comparison: Compared to traditional insurance, Snapshot rewards good driving behavior directly with lower rates. Unlike some competitors, Snapshot doesn't increase your rates if your driving isn't perfect, it just won't give you the maximum discount.

Price: The device is free, and the potential savings can range from a few dollars to hundreds of dollars per year.

Product Recommendation 2: State Farm Drive Safe & Save

Description: Similar to Progressive Snapshot, State Farm Drive Safe & Save is a usage-based program that uses a mobile app to track your driving habits. It monitors things like acceleration, braking, turning, and speed.

Use Case: A good option for State Farm customers who want to save money by demonstrating safe driving habits.

Comparison: Drive Safe & Save uses a mobile app, which some users may find more convenient than plugging in a device. However, the app relies on your smartphone's sensors, which can sometimes be less accurate than a dedicated device. Unlike some competitors, State Farm is known for its strong customer service.

Price: The app is free to download, and potential discounts vary based on driving behavior.

Product Recommendation 3: Geico DriveEasy

Description: Geico DriveEasy is another app-based program that tracks driving habits. It focuses on things like hard braking, phone use while driving, and time of day.

Use Case: Suitable for Geico customers looking for a mobile-based option to potentially lower their insurance rates by showcasing safe driving.

Comparison: DriveEasy is entirely app-based. Geico is generally known for its competitive pricing. The app tracks phone usage while driving which could be a deterrent for some drivers.

Price: Free to download the app. Discounts vary based on driving performance.

Product Comparison Table

| Feature | Progressive Snapshot | State Farm Drive Safe & Save | Geico DriveEasy |

|---|---|---|---|

| Tracking Method | Device | Mobile App | Mobile App |

| Focus | Speeding, Hard Braking, Nighttime Driving | Acceleration, Braking, Turning, Speed | Hard Braking, Phone Use While Driving, Time of Day |

| Customer Service Reputation | Good | Excellent | Good |

| Potential Savings | Significant | Variable | Variable |

Choosing the Right Car Insurance Policy Considering Your Needs

Ultimately, the best car insurance policy for you depends on your individual circumstances. Think about your budget, your driving habits, and your risk tolerance. Don't be afraid to talk to an insurance agent to get personalized advice. They can help you understand your options and choose the right coverage for your needs.

Remember to review your policy regularly and make sure it still meets your needs. As your life changes, your insurance needs may also change. For example, if you buy a new car or move to a new location, you'll need to update your policy.

And finally, drive safely! The best way to avoid accidents and keep your insurance rates low is to be a responsible driver.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)