Financial Planning After a Car Accident: Managing Your Resources

Understanding the Financial Impact of a Car Accident Insurance Claims and Settlements

Okay, so you've been in a car accident. First of all, I hope you're okay. Seriously, your health is the priority. But once you've started the healing process, it's time to face the financial music. Car accidents can throw a serious wrench into your finances, leaving you with medical bills, repair costs, lost wages, and a whole lot of stress. Let's break down how to navigate this financial maze, focusing on managing your resources effectively.

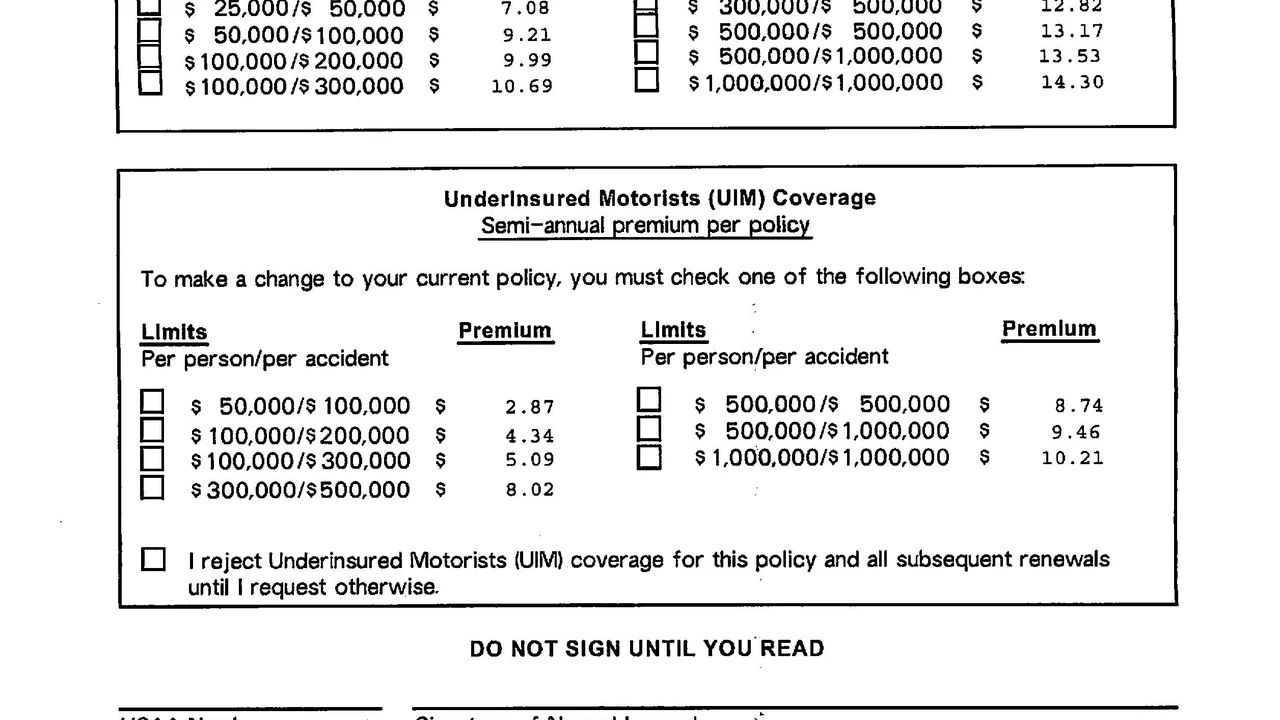

First things first: insurance. Your car insurance policy is your first line of defense. Understand your coverage. What's your deductible? What are your liability limits? What about uninsured/underinsured motorist coverage? These details matter. Contact your insurance company immediately to report the accident and start the claims process. Document everything: photos of the damage, police reports, medical records, and any communication with the insurance company. Keep a detailed log of your expenses related to the accident. This will be crucial when negotiating a settlement.

The claims process can be lengthy and frustrating. Be patient, but persistent. Don't be afraid to ask questions and challenge any denials or lowball offers. Consider consulting with a personal injury attorney, especially if you've suffered serious injuries or if the insurance company is being difficult. An attorney can help you understand your rights and negotiate a fair settlement.

Settlements can come in different forms. You might receive a lump-sum payment or structured payments over time. Think carefully about which option is best for you. A lump sum provides immediate access to funds, but you'll be responsible for managing it wisely. Structured payments offer long-term financial security, but you won't have as much flexibility.

Budgeting After a Car Accident Income Replacement and Expense Management

Alright, now let's talk about budgeting. A car accident can significantly impact your income, especially if you're unable to work due to injuries. Start by creating a detailed budget that reflects your current income and expenses. Identify areas where you can cut back on spending. This might involve temporarily suspending non-essential subscriptions, reducing your entertainment budget, or finding cheaper alternatives for groceries.

If you're unable to work, explore options for income replacement. This might include short-term disability insurance, workers' compensation (if the accident occurred while you were working), or unemployment benefits. Contact your employer and the relevant government agencies to learn about your eligibility.

Prioritize your expenses. Focus on essential needs like housing, food, transportation, and medical care. Communicate with your creditors and explain your situation. They might be willing to offer temporary payment arrangements or deferments. Avoid taking on new debt unless absolutely necessary.

Consider setting up a dedicated savings account specifically for accident-related expenses. This will help you keep track of your spending and avoid dipping into your emergency fund for other purposes.

Medical Bills and Healthcare Costs After a Car Wreck Negotiating and Payment Plans

Medical bills are often the biggest financial burden after a car accident. Even with health insurance, you may still face significant out-of-pocket costs for deductibles, co-pays, and uncovered services. Don't panic! There are ways to manage these expenses.

First, review your medical bills carefully for any errors or discrepancies. Contact the billing department of each healthcare provider and ask for an itemized statement. If you find any mistakes, report them immediately.

Negotiate with your healthcare providers. Many hospitals and doctors are willing to offer discounts or payment plans, especially if you're uninsured or underinsured. Don't be afraid to ask! You might be surprised at how much you can save.

Explore options for financial assistance. Many hospitals have programs that provide free or reduced-cost care to low-income patients. You can also research charitable organizations that offer financial assistance to car accident victims.

Consider setting up a payment plan with your healthcare providers. This will allow you to spread your payments over time, making them more manageable. Be sure to agree on a payment plan that you can realistically afford.

Debt Management Strategies After a Car Crash Credit Counseling and Consolidation

If you're struggling to manage your debt after a car accident, consider seeking professional help. A credit counselor can help you develop a budget, negotiate with your creditors, and explore options for debt consolidation or debt management plans. Be sure to choose a reputable credit counseling agency that is accredited by the National Foundation for Credit Counseling (NFCC).

Debt consolidation involves taking out a new loan to pay off your existing debts. This can simplify your finances and potentially lower your interest rate. However, be careful to avoid high-interest debt consolidation loans that could make your situation worse.

A debt management plan (DMP) is a structured repayment plan that is negotiated by a credit counseling agency with your creditors. Under a DMP, you make a single monthly payment to the credit counseling agency, which then distributes the funds to your creditors. DMPs can help you lower your interest rates and avoid late fees.

Avoid using high-interest credit cards to cover accident-related expenses. This can quickly lead to a cycle of debt that is difficult to escape.

Investing Settlement Money After a Car Accident Long Term Financial Security

If you receive a settlement from your car accident, it's important to manage it wisely. Don't blow it all on frivolous purchases. Instead, consider investing a portion of your settlement to secure your long-term financial future.

Work with a financial advisor to develop an investment strategy that aligns with your goals and risk tolerance. Consider diversifying your investments across different asset classes, such as stocks, bonds, and real estate. This will help you reduce your risk and maximize your potential returns.

If you have significant medical expenses, consider setting up a special needs trust. This type of trust can protect your settlement money from being counted as assets for Medicaid eligibility purposes.

Don't forget to pay your taxes. Settlement money may be taxable, depending on the nature of the claim. Consult with a tax advisor to understand your tax obligations.

Financial Planning Tools and Resources for Car Accident Victims Online Calculators and Apps

There are many online tools and resources available to help car accident victims manage their finances. Here are a few examples:

- Budgeting Apps: Mint, YNAB (You Need A Budget), Personal Capital. These apps help track spending, create budgets, and monitor financial progress.

- Debt Management Calculators: Many websites offer free debt management calculators that can help you estimate your debt repayment options.

- Insurance Claim Tracking Apps: Some insurance companies offer mobile apps that allow you to track the status of your claim and communicate with your adjuster.

- Financial Planning Websites: NerdWallet, The Balance, and Investopedia offer a wealth of information on personal finance topics, including budgeting, debt management, and investing.

Specific Product Recommendations for Financial Recovery Post-Accident

Let's talk about some specific products that can really help you get back on your feet financially after an accident. I'm going to be upfront; I'm not endorsing anything I haven't researched and think could genuinely be useful.

Budgeting Software: YNAB (You Need a Budget)

What it is: YNAB isn't just a budgeting app; it's a budgeting *philosophy*. It forces you to be proactive about your spending, allocating every dollar you have to a specific purpose before you spend it. This is especially crucial when you're dealing with unexpected expenses and income fluctuations.

Use Case: Imagine you get a settlement check. Instead of just letting it sit in your bank account, YNAB helps you allocate it. Maybe a chunk goes to paying down medical debt, another portion gets earmarked for car repairs, and the rest gets put into an emergency fund. It provides a clear picture of where your money is going and ensures you're prioritizing the most important needs.

Comparison: Compared to Mint (which is great for tracking past spending) or Personal Capital (which is geared more towards investment management), YNAB is laser-focused on proactive budgeting. It requires more effort upfront, but the payoff in terms of financial control is significant.

Price: Approximately $14.99/month or $99/year. It's an investment, but if it helps you avoid debt and manage your settlement wisely, it's worth it.

Credit Counseling Services: NFCC-Accredited Agencies

What it is: Non-profit credit counseling agencies can provide invaluable support in navigating debt and creating a repayment plan. Look for agencies accredited by the National Foundation for Credit Counseling (NFCC) to ensure they're legitimate and offer unbiased advice.

Use Case: If you're overwhelmed by medical debt and struggling to make payments, a credit counselor can negotiate with your creditors on your behalf, potentially lowering interest rates or setting up a manageable payment plan. They can also help you develop a budget and avoid falling further into debt.

Comparison: Unlike for-profit debt settlement companies, NFCC-accredited agencies focus on education and sustainable solutions. They won't promise to magically eliminate your debt, but they'll provide the tools and support you need to get back on track.

Price: Initial consultations are often free. Debt management plans typically involve a small monthly fee, but it's a fraction of what you'd pay in interest and late fees without assistance.

Personal Finance Books: "The Total Money Makeover" by Dave Ramsey

What it is: This book offers a straightforward, no-nonsense approach to getting out of debt and building wealth. While some of Ramsey's advice is controversial (like his aversion to all debt), his core principles of budgeting, saving, and debt snowballing are solid.

Use Case: If you're feeling lost and overwhelmed by your financial situation, this book can provide a clear roadmap. It's particularly helpful for people who are motivated by a step-by-step approach and a strong sense of discipline.

Comparison: Compared to books that focus on investing or financial planning, "The Total Money Makeover" is all about getting your financial house in order. It's a great starting point for anyone who's struggling with debt.

Price: Around $20, a very worthwhile investment in your financial literacy.

Tax Software: TurboTax or H&R Block

What it is: Tax software simplifies the process of filing your taxes, especially when you have complex situations like medical expenses or settlement income. These programs guide you through the steps, identify potential deductions, and ensure you're complying with tax laws.

Use Case: After a car accident, you might have deductions related to medical expenses, legal fees, or property loss. Tax software can help you accurately claim these deductions and potentially reduce your tax liability.

Comparison: TurboTax and H&R Block are both popular options with similar features. Choose the one that you find easiest to use and that offers the level of support you need.

Price: Ranges from free (for simple returns) to around $100 (for more complex situations). The cost is often offset by the tax savings you'll achieve by accurately claiming deductions.

Building an Emergency Fund After an Accident Rainy Day Savings

Building an emergency fund is always a good idea, but it's especially crucial after a car accident. An emergency fund provides a financial cushion to cover unexpected expenses, such as medical bills, car repairs, or lost wages. Aim to save at least three to six months' worth of living expenses in a readily accessible savings account.

Start small. Even saving a few dollars each week can make a difference over time. Automate your savings by setting up a recurring transfer from your checking account to your savings account.

Consider using a high-yield savings account to maximize your earnings. These accounts typically offer higher interest rates than traditional savings accounts.

Legal Advice and Representation After a Car Crash Finding the Right Attorney

If you've been seriously injured in a car accident, it's important to seek legal advice from a qualified attorney. An attorney can help you understand your rights, negotiate with the insurance company, and pursue a lawsuit if necessary. Choose an attorney who specializes in personal injury law and has a proven track record of success.

Ask for referrals from friends, family, or other professionals. Check online reviews and ratings. Schedule consultations with several attorneys before making a decision. Be sure to ask about their fees and payment arrangements.

Long-Term Financial Goals After a Car Accident Retirement Planning

Even after a car accident, it's important to continue planning for your long-term financial goals, such as retirement. If you've received a settlement, consider using a portion of it to fund your retirement accounts.

Contribute to your 401(k) or other retirement plan at work. Take advantage of any employer matching contributions. Consider opening a Roth IRA or traditional IRA.

Work with a financial advisor to develop a retirement plan that meets your needs and goals. Be sure to consider your risk tolerance, time horizon, and investment objectives.

Staying Positive and Motivated During Financial Recovery Mindset Matters

Recovering financially from a car accident can be a long and challenging process. It's important to stay positive and motivated. Focus on your goals and celebrate your progress along the way. Surround yourself with supportive friends and family. Remember that you're not alone. Many people have successfully overcome similar challenges.

Seek professional help if you're struggling with stress, anxiety, or depression. Mental health is just as important as physical health.

Practice self-care. Take time for activities that you enjoy and that help you relax. This will help you manage stress and maintain a positive outlook.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)