Understanding Uninsured and Underinsured Motorist Coverage

What is Uninsured Motorist (UM) Coverage and Why You Need It

Let's face it, nobody *wants* to think about getting into a car accident. But statistically, it happens. And what's even worse than the accident itself is finding out the other driver has no insurance, or worse, flees the scene. That's where Uninsured Motorist (UM) coverage comes in. Think of it as your safety net when the other guy drops the ball (or, you know, the insurance card).

UM coverage protects you, and often your passengers, if you're hit by a driver who doesn't have insurance. It covers your medical bills, lost wages, and even pain and suffering, up to the limits of your policy. It's like your own insurance company steps in to cover you as if the uninsured driver *did* have insurance. Pretty important, right?

Underinsured Motorist (UIM) Coverage Explained: Filling the Gaps in Coverage

Okay, so what about Underinsured Motorist (UIM) coverage? This is a bit trickier, but equally important. UIM kicks in when the at-fault driver *does* have insurance, but their coverage limits aren't enough to cover all your damages. Imagine you're seriously injured in an accident, and your medical bills alone are $100,000. The other driver only has $50,000 in liability coverage. UIM coverage can help bridge that $50,000 gap.

The way it works is that your insurance company essentially pays you the difference between the at-fault driver's policy limits and your UIM policy limits, up to the total amount of your UIM coverage. So, if you have $100,000 in UIM coverage, your insurance would pay the remaining $50,000 to cover your medical bills (assuming your UIM coverage hasn't been used for other expenses). It's all about making sure you're fully compensated for your injuries and losses.

Real Life Scenarios: When UM and UIM Coverage Save the Day

Let's paint a few pictures. Imagine you're driving home from work, and a distracted driver runs a red light, T-boning your car. You suffer whiplash and need physical therapy. Turns out, the driver is uninsured. Without UM coverage, you'd be stuck paying those medical bills yourself. But with UM, your insurance company covers those costs, plus any lost wages from missing work.

Another scenario: you're rear-ended on the highway. You require surgery and ongoing medical care. The other driver has insurance, but only the state minimum, which barely scratches the surface of your expenses. UIM coverage steps in to pay the difference, preventing you from being financially devastated by someone else's negligence.

Comparing UM and UIM Coverage: Policy Limits and What to Consider

When choosing UM and UIM coverage, policy limits are crucial. Think about it: what's the maximum amount your insurance company will pay out in the event of an accident? Generally, it's a good idea to match your UM/UIM coverage to your liability coverage. If you have $100,000 in liability coverage, aim for $100,000 in UM/UIM coverage as well.

Consider your assets and income. The more you have to lose, the more coverage you need. Also, think about the risks in your area. Are there a lot of uninsured drivers? If so, higher UM/UIM coverage is even more important. Talk to your insurance agent to assess your specific needs and choose the right coverage levels.

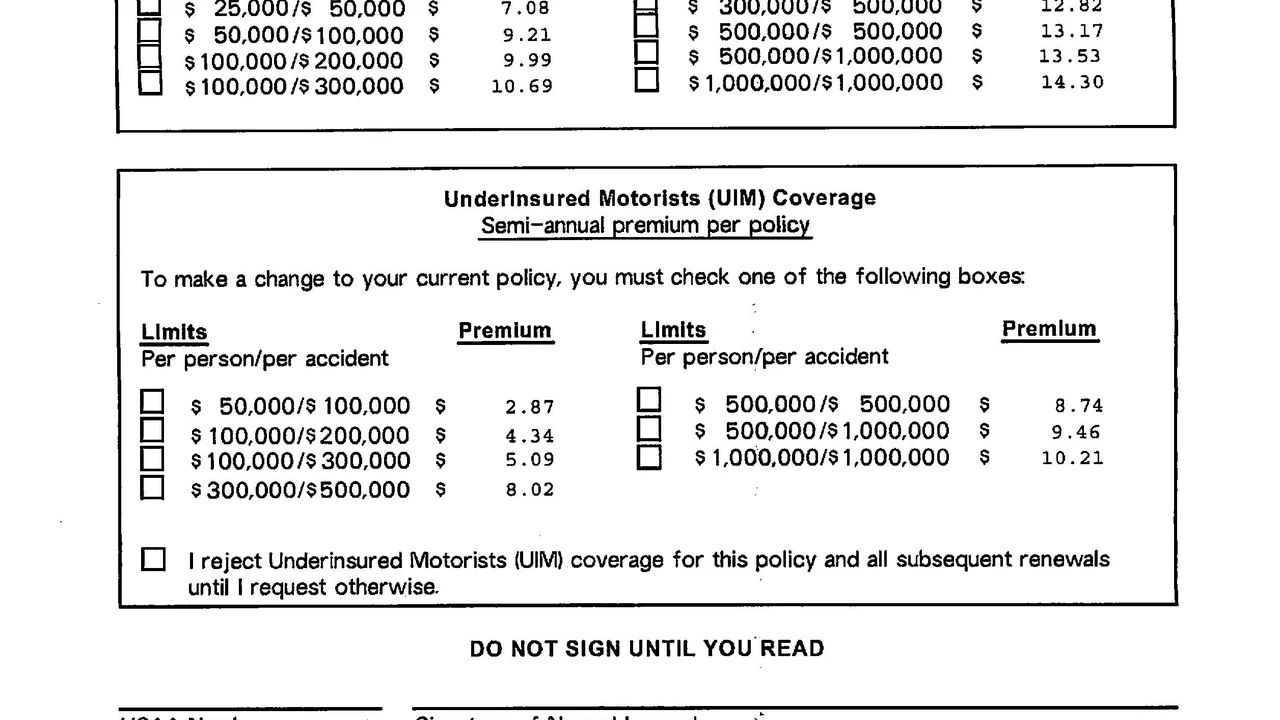

Stacking vs Non-Stacking UM/UIM Coverage: Maximizing Your Protection

Here's a term you might hear: "stacking." Stacking allows you to combine the UM/UIM coverage limits for multiple vehicles on your policy. For example, if you have two cars with $50,000 UM coverage each and stacking is allowed, you effectively have $100,000 in UM coverage available if you're injured by an uninsured driver. Not all states allow stacking, so check your local laws. If it's available, it can significantly increase your protection.

Non-stacking, on the other hand, means you can only use the UM/UIM coverage from the vehicle involved in the accident, regardless of how many vehicles you have on your policy. Stacking is generally more expensive, but it offers greater peace of mind.

Finding the Best UM and UIM Coverage Rates: Shopping Around and Getting Quotes

Don't just stick with the first insurance quote you get! Shop around and compare rates from multiple insurance companies. Online quote comparison tools can be helpful, but also consider contacting independent insurance agents who can get quotes from several different companies. Be sure to compare the *coverage* as well as the price. A cheaper policy might not offer the same level of protection.

Factors that affect your UM/UIM rates include your driving record, the type of car you drive, and your location. Also, consider bundling your auto insurance with your home or renters insurance to save money. And ask about discounts for safe driving or having anti-theft devices in your car.

Understanding UM and UIM Policy Exclusions: What's Not Covered

It's crucial to know what your UM/UIM policy *doesn't* cover. Common exclusions include:

- Injuries sustained while committing a crime.

- Injuries sustained while using your vehicle for commercial purposes (unless you have a commercial auto policy).

- Injuries sustained if you intentionally cause the accident.

- Injuries to family members living in your household who have their own auto insurance policy with UM/UIM coverage.

Read your policy carefully and ask your insurance agent about any exclusions you don't understand. Knowing what's *not* covered is just as important as knowing what *is* covered.

Dealing with Insurance Companies After an Accident: Making a UM/UIM Claim

Okay, so you've been in an accident with an uninsured or underinsured driver. Now what? First, report the accident to the police and your insurance company immediately. Gather as much information as possible about the other driver, including their name, address, and license plate number (even if they don't have insurance). Take photos of the damage to your vehicles and the accident scene.

When filing a UM/UIM claim, be prepared to provide documentation of your injuries and losses, including medical bills, lost wage statements, and repair estimates. Your insurance company will investigate the accident to determine fault and the extent of your damages. Be patient, but don't be afraid to advocate for yourself. If you feel your claim is being unfairly denied or undervalued, consider consulting with an attorney.

Recommended Uninsured/Underinsured Motorist Coverage Products and Their Use Cases

Alright, let's talk about some insurance companies that are known for their good UM/UIM coverage options. Keep in mind that availability and pricing can vary depending on your location and individual circumstances, so always get a personalized quote.

- State Farm: State Farm is a large, well-established insurer with a reputation for good customer service. They offer a range of UM/UIM coverage options, and their agents can help you customize a policy to fit your specific needs. Use Case: Good for families and those looking for a reliable, established insurer. Average cost for UM/UIM coverage: $150-$300 annually, depending on coverage limits.

- GEICO: GEICO is known for its competitive pricing and online convenience. They offer UM/UIM coverage in most states and have a user-friendly website and mobile app. Use Case: Ideal for budget-conscious drivers who prefer managing their insurance online. Average cost for UM/UIM coverage: $120-$250 annually, depending on coverage limits.

- Progressive: Progressive offers a variety of coverage options and discounts, and they are known for their "Name Your Price" tool, which allows you to set your budget and see what coverage options are available. Use Case: Suitable for drivers who want flexibility and the ability to customize their policy. Average cost for UM/UIM coverage: $130-$280 annually, depending on coverage limits.

- Allstate: Allstate is another large, reputable insurer with a wide range of coverage options. They offer UM/UIM coverage as part of their standard auto insurance policies and have a network of local agents. Use Case: A good choice for those who prefer working with a local agent and want comprehensive coverage. Average cost for UM/UIM coverage: $160-$320 annually, depending on coverage limits.

Comparing UM/UIM Products: Features, Benefits, and Price Points

When comparing UM/UIM products, consider the following factors:

- Coverage Limits: What's the maximum amount the policy will pay out?

- Deductible: Do you have to pay a deductible before the coverage kicks in?

- Stacking Options: Is stacking allowed in your state and does the policy offer it?

- Uninsured Property Damage (UMPD): Does the policy also cover damage to your vehicle caused by an uninsured driver?

- Customer Service: Does the insurer have a good reputation for handling claims fairly and efficiently?

- Price: How does the cost of the policy compare to other options with similar coverage?

Remember to read the fine print and ask questions before making a decision. Don't be afraid to negotiate or shop around for a better deal.

Understanding the Costs of UM/UIM Coverage

The cost of UM/UIM coverage varies depending on several factors, including:

- Your Location: States with higher rates of uninsured drivers typically have higher UM/UIM premiums.

- Your Driving Record: A history of accidents or traffic violations can increase your premiums.

- Your Vehicle: The type of car you drive can also affect your rates.

- Coverage Limits: Higher coverage limits mean higher premiums.

- Deductible: A higher deductible can lower your premiums, but you'll have to pay more out-of-pocket if you file a claim.

On average, UM/UIM coverage adds between $50 and $300 per year to your auto insurance premium. While it may seem like an extra expense, it's a worthwhile investment that can protect you from significant financial losses in the event of an accident with an uninsured or underinsured driver.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)